Simplifying Monetary Policy: How Central Banks Regulate the Economy

Think of monetary policy as the remote control for the economy. Just like you use a remote to adjust the volume and channels on your TV, the central bank uses monetary policy to control the money supply and interest rates. By finding the right balance, they aim to keep prices stable and the economy running smoothly, just like you adjust the settings on your TV for the best viewing experience.

Let's understand monetary policy: its definition and crucial role in regulating a country's economy.

What Is Monetary Policy?

Monetary policy involves the measures taken by a central bank to control the money supply and interest rates in an economy. Its main objectives include ensuring price stability, supporting sustainable economic growth, and achieving full employment. Central banks utilize tools like adjusting interest rates, conducting open market operations, and setting reserve requirements to manage the amount of money circulating in the economy.

Through the implementation of this policy, central banks can increase or decrease the amount of money and credit in circulation, aiming to maintain desirable levels of inflation, economic growth, and employment. This effort ensures that these key economic indicators remain within the desired range.

The Nepal Rastra Bank (NRB) is responsible for the implementation of monetary policy in Nepal, as mandated by the Nepal Rastra Bank Act of 2002. Since the fiscal year 2002/03, the NRB has been actively involved in formulating and publicly announcing its monetary policy. Furthermore, the bank conducts half-yearly reviews, starting from 2003/04, and quarterly reviews, since 2016/17, to thoroughly assess the economic and financial situation and make appropriate policy adjustments based on the findings of these reviews.

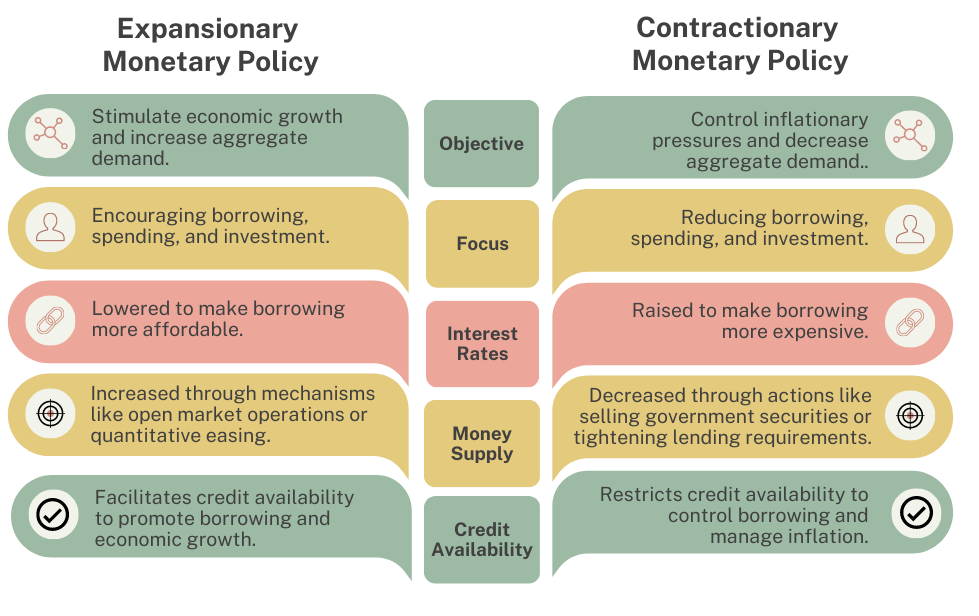

Monetary policy can be classified into two distinct approaches: expansionary and contractionary.

Expansionary Monetary Policy vs Contractionary Monetary Policy

Expansionary monetary policy is employed to boost the amount of money in circulation and encourage inflation, while contractionary monetary policy is utilized to reduce inflationary pressures by decreasing the money supply in the economy.

The choice between expansionary and contractionary monetary policy depends on economic conditions and policy objectives. Expansionary policy is used during economy downturns, while contractionary policy controls inflation.

The choice between expansionary and contractionary monetary policy depends on economic conditions and policy objectives. Expansionary policy is used during economy downturns, while contractionary policy controls inflation.

In the context of Nepal, the Nepal Rastra Bank (NRB) performs the crucial role of implementing the expansionary or contractionary monetary policy as per requirement. To effectively accomplish this task, the NRB employs a range of monetary policy instruments, both quantitative and qualitative in nature. These instruments, such as the Cash Reserve Ratio (CRR), Statutory Liquidity Ratio (SLR), Bank Rate, Repo Rate, Reverse Repo Rate, Open Market Operations, and more. By skillfully utilizing these tools, the NRB actively shapes and guides the economy towards its desired objectives.

Tools of Monetary Policy

To gain a better understanding of the monetary policy instruments employed by the Nepal Rastra Bank (NRB), let's analyze the quantitative and qualitative measures individually.

Quantitative Methods

Quantitative instruments, also known as general tools, are employed by the NRB to effectively manage the quantity of money circulating in the economy. These instruments have a direct impact on the overall volume of bank credit available. By utilizing these tools, the NRB aims to control over the total credit supply in the economy, indirectly influencing economic factors such as interest rates and liquidity.

Interest Rate Adjustment

Imagine NRB as a powerful conductor of interest rates. It has a special tool called the bank rate, which is like interest charged to banks for short-term loans. Now, here's the interesting part: when the NRB increases the bank rate, it starts a chain reaction. The cost of borrowing for banks goes up, so they raise the interest rates they charge their customers.

As a result, borrowing becomes more expensive for everyone, and there's less money available in the economy. It's like a fascinating dance of numbers and decisions by the NRB that affects how much we pay to borrow money from banks.

Legal Reserve Ratios

NRB plays a crucial role in shaping the economy through reserve requirements like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). When these requirements are raised, it restricts the amount of money banks can lend, resulting in a tighter money supply.

Conversely, lowering these requirements increases lending capacity and stimulates economic activity. The NRB's decisions on reserve requirements have a direct impact on the availability of funds in banks and the overall health of the economy.

Open Market Operations (OMO)

Open market operations refer to the sale and purchase of securities by the Nepal Rastra Bank (NRB) in the money market, serving as a widely utilized tool of the NRB's monetary policy. These operations are employed to shape the term and structure of interest rates, stabilize the market for government securities, and address any shortage and excess of funds in the banking channel.

When the NRB sells securities in the money market, banks, financial institutions, and even individuals purchase them. Consequently, the existing money supply diminishes as funds are transferred from these entities to the NRB. Conversely, when the NRB buys securities from banks, the selling banks receive the equivalent amount they had initially invested with the NRB.

Repo Rate

The repo rate refers to the rate at which banks can borrow funds from the NRB offering their securities as collateral. This helps banks address temporary liquidity shortages or fulfill statutory requirements. Essentially, it serves as a key tool used by the NRB to provide short-term liquidity support to banks and facilitate stability in the market.

When the NRB raises the repo rate, borrowing becomes costlier for banks, which can lead to reduced liquidity and potential economic slowdown. Conversely, when the NRB lowers the repo rate, borrowing becomes cheaper, increasing liquidity and potentially boosting economic activity.

Reverse Repo Rate

The reverse repo rate, a monetary policy tool employed by central banks, regulates liquidity in the financial system. It represents the rate at which the central bank borrows funds from commercial banks and other financial institutions when there is excess liquidity in the market by selling securities, with an agreement to repurchase them later.

When the central bank raises the reverse repo rate, it encourages banks to deposit excess funds with the central bank, reducing liquidity and curbing inflationary pressures. Conversely, a decrease in the reverse repo rate prompts banks to lend more, increasing liquidity and stimulating economic activity. It is essential to note that the impact of the reverse repo rate can vary depending on the country and economic conditions.

Qualitative Methods

Qualitative instruments, also known as selective instruments in monetary policy, provide the central bank with the ability to differentiate between different credit applications. For example, they may choose to favor lending to small and medium-sized enterprises (SMEs) to promote entrepreneurship and job creation, while imposing stricter regulations on speculative or risky investments. These instruments have a notable impact on borrowers and lenders, influencing the allocation of credit throughout the economy. By utilizing qualitative instruments, the central bank can actively steer economic activities towards areas that contribute to overall growth and stability, fostering a robust and inclusive financial landscape.

Central banks implement a range of specific credit control measures to regulate the flow of credit in the economy. Let’s explore in details:

Revise the Marginal Requirement

Marginal Requirement refers to the specific condition in the realm of finance and lending where a loan is approved and granted based on a certain proportion or fraction of the value of the collateral provided by the borrower. This means that the lender evaluates the collateral's worth and agrees to extend a loan amount that is calculated as a percentage of that assessed value.

For instance, if the marginal requirement is set at 70%, by providing collateral worth Rs. 100, you can access a loan of Rs. 70.

Suppose the central bank of a country believes that the manufacturing sector requires a boost in credit availability. In response, the central bank decides to lower the collateral requirements, allowing up to 80-90% of the loan to be allocated to manufacturing businesses. In this manner, central banks utilize this mechanism to impact the money supply in different sectors, effectively shaping credit allocation according to their economic priorities.

Regulation of Consumer Credit

Regulating consumers' credit supply relies on establishing predefined parameters for purchasing consumer goods through installment plans. These predetermined features, such as fixed installment amounts, down payments, and loan durations, effectively contribute to monitoring credit and stabilizing inflation within the country.

For instance, if the down payment is increased for certain products, it acts as a disincentive for potential buyers, discouraging them from making the purchase.

Moral Suasion

Moral suasion, also referred to as moral persuasion or moral guidance, stands as an unconventional monetary policy tool utilized by central banks to influence the actions of financial institutions and other economic players. In contrast to traditional measure, moral suasion operates on the principle of informal communication and cooperation, rather than imposing direct regulatory measures.

The fundamental idea behind moral suasion is rooted in the central bank's capacity to rely on its credibility, reputation, and persuasive powers to encourage banks and financial institutions to adopt specific behaviors or policy measures. Through methods like public statements, private meetings, or informal discussions, the central bank articulates its expectations and recommendations to the financial sector and other relevant stakeholders, aiming to steer their actions in line with desired outcomes.

Final Thoughts

In this way central banks exert significant control over the entire economy by managing interest rates and the money supply. As individuals participating in the economy, it is crucial for us to be well-informed about monetary policy and its effects on our consumption habits. By grasping the fundamental concepts behind monetary policy and its tools, we can gain a comprehensive understanding of its economic impact overall. This knowledge empowers us, whether we are investors, students, businesspeople, or professionals in any field, to make informed decisions that lead to better outcomes.